HCI's surging growth props up global converged systems market

Wed, 3rd Apr 2019

New research from the International Data Corporation (IDC) has found the global converged system market to be in good stead.

According to IDC, market revenue increased 14.8% year over year to reach US$4.15 billion during the fourth quarter of 2018 (4Q18).

"Hyperconverged infrastructure demand remains the primary driver of converged systems market growth," says IDC infrastructure platforms and technologies research manager Sebastian Lagana.

"As HCI solutions are increasingly capable of operating business-critical workloads while reducing data center complexity and promoting affordability, the segment will continue to expand its share of the overall converged systems market."

IDC has broken the overall converged systems market into three categories – certified reference systems - integrated infrastructure, integrated platforms, and hyperconverged systems.

The certified reference systems - integrated infrastructure market generated $1.6 billion in revenue during the fourth quarter, which represents a year-over-year decline of 6.4% and 38.6% of total converged systems revenue

Integrated platforms sales declined 8.4% year over year in 4Q18, generating revenue of $619 million. This was 14.9% of the total converged systems market revenue.

Propping the market up was hyperconverged systems, as sales grew 57.2% year over year during the fourth quarter, generating $1.9 billion in revenue. This amounted to 46.5% of the total converged systems market.

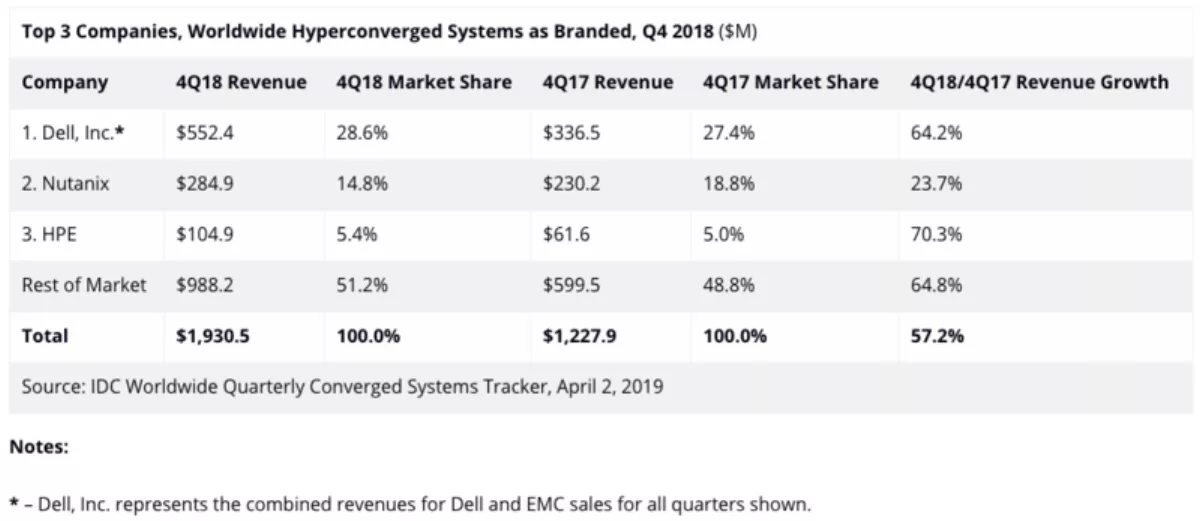

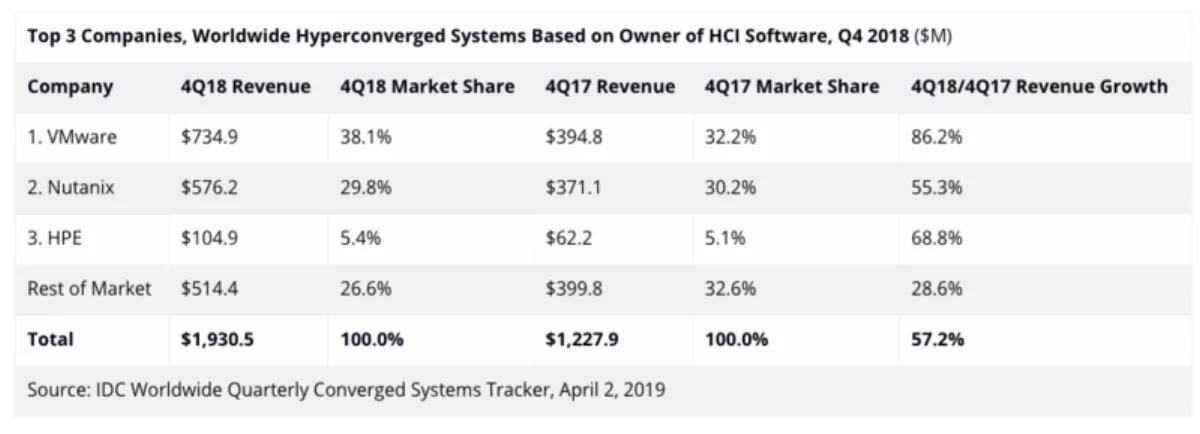

IDC uses two ways to rank technology suppliers within the hyperconverged systems market - by the brand of the hyperconverged solution or by the owner of the software providing the core hyperconverged capabilities.

Rankings based on a branded view of the market can be found in the first table, while rankings based on the owner of the hyperconverged software can be found in the second table. Both tables include all the same software and hardware, summing to the same market size.

As it relates to the branded view of the hyperconverged systems market, Dell, Inc. was the largest supplier in 4Q18 with $552.4 million in revenue and a 28.6% share of the market. Nutanix generated $284.9 million in branded revenue, which represents 14.8% of the total HCI market during the quarter and 49% of the total HCI revenue generated through sales of systems running Nutanix software. HPE was the third largest branded HCI vendor with $104.9 million in revenue and 5.4% market share.

From the software ownership view of the market, systems running VMware hyperconverged software represented $734.9 million in total fourth quarter vendor revenue or 38.1% of the total market. Systems running Nutanix hyperconverged software represented $576.2 million in fourth quarter vendor revenue or 29.8% of the total market. Both amounts represent sales of all HCI software and hardware regardless of how it was branded.