Record revenues from servers selling like hot cakes

Wed, 12th Dec 2018The relentless demand for data has resulted in another robust quarter for the global server market.

According to the International Data Corporation (IDC), vendor revenue in the global server market surged 37.7 percent year-over-year to reach US$23.4 billion during the third quarter of 2018 (3Q18). Meanwhile, global server shipments increased 18.3 percent year-over-year to hit 3.2 million units in the quarter.

"The worldwide server market once again generated strong revenue and unit shipment growth due to an ongoing enterprise refresh cycle and continued demand from cloud service providers," says IDC Infrastructure Platforms and Technologies research manager Sebastian Lagana.

This is the fifth consecutive quarter of double-digit revenue growth for the server market, with 3Q18 being its highest total revenue in a single quarter ever.

Volume server revenue increased by 40.2 percent to $20 billion, while midrange server revenue grew 39.4 percent to $2 billion. High-end systems grew 6.9 percent to $1.3 billion.

"Enterprise infrastructure requirements from resource intensive next-generation applications support increasingly rich configurations, ensuring average selling prices (ASPs) remain elevated against the year-ago quarter. At the same time, hyperscalers continue to upgrade and expand their data center capabilities," says Lagana.

Looking at the market from a geographical point of view, Asia Pacific (excluding Japan) was the fastest growing region over the quarter having posted 46.5 percent year-over-year revenue growth

The United States is nipping on its heels having posted 43.7 percent growth in the quarter, followed somewhat further back by Europe, the Middle East, and Africa (EMEA) with 24.5 percent, Canada on 20 percent, Japan on 14 percent, and Latin America on 7.7 percent. China alone saw its 3Q18 vendor revenues surge by 67.1 percent year-over-year.

In terms of the types of servers, demand for x86 servers increased 41 percent in 3Q18 to reach $21.8 billion in revenues. Non-x86 servers on the other hand grew just 3.9 percent year-over-year to reach $1.6 billion.

The vendors

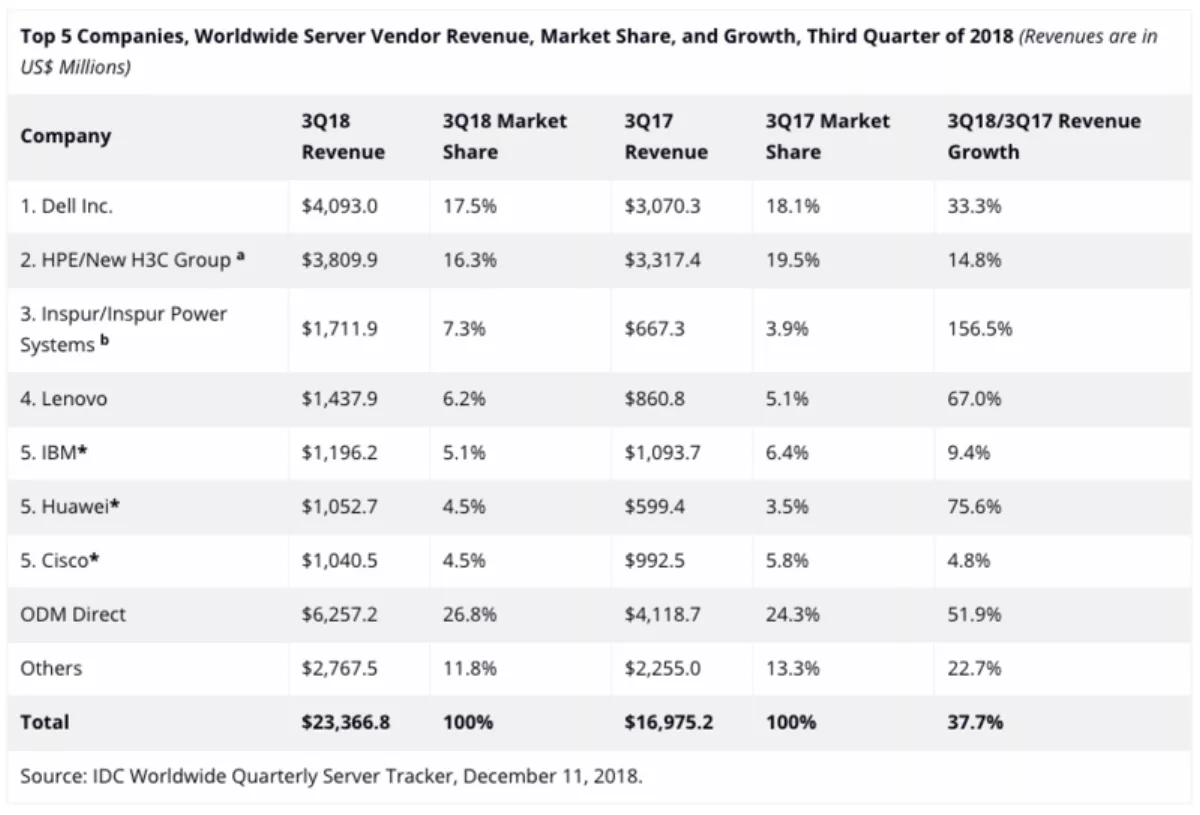

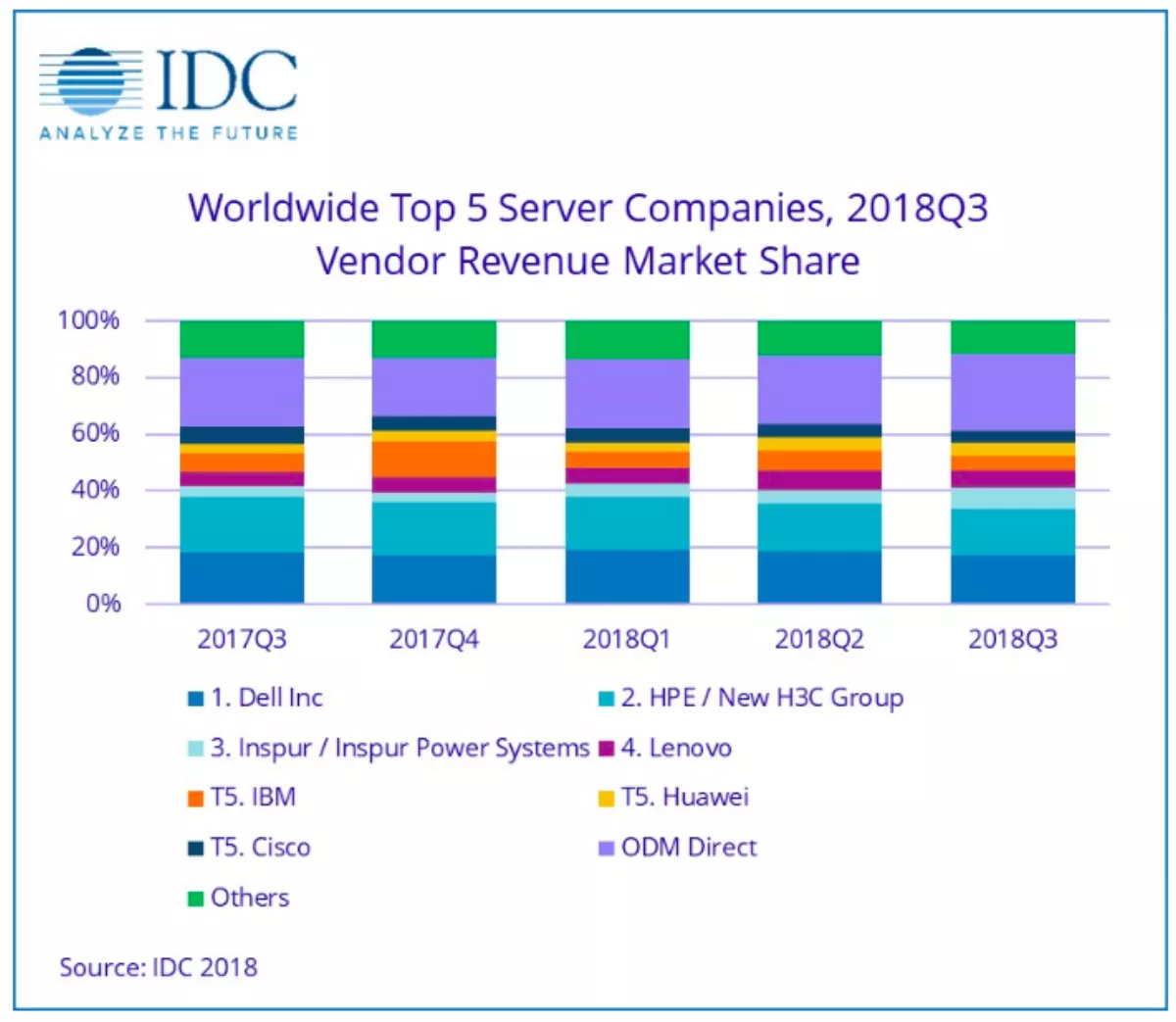

Dell held on to its position at the top of the pile with 17.5 percent piece of the total worldwide server market revenue, having grown by 33 percent in the quarter. Dell also led the market in terms of unit shipments, making up for 17.6 percent of all units shipped over the quarter.

HPE/New H3C Group was the second largest supplier with a 16.3 percent share of the market, growing 14.8 percent. Inspur/Inspur Power Systems took third position in the market with a share of 7.3% while the new joint venture contributed to 156.5% growth year over year.

Lenovo came in fourth with a share of 6.2 percent and underwent massive growth with 67 percent. IBM, Huawei, and Cisco rounded out the top five, all statistically tied* with vendor revenue shares of 5.1 percent, 4.5 percent, and 4.5 percent respectively.

The ODM Direct group of vendors also saw substantial growth, having expanded its collective revenue by 51.9 percent year-over-year to reach almost $6.3 billion.

Notes:

* IDC declares a statistical tie in the worldwide server market when there is a difference of one percent or less in the share of revenues or shipments among two or more vendors.

a Due to the existing joint venture between HPE and the New H3C Group, IDC will be reporting external market share on a global level for HPE and New H3C Group as "HPE/New H3C Group" starting from 2Q 2016.

b Due to the existing joint venture between IBM and Inspur, IDC will be reporting external market share on a global level for Inspur and Inspur Power Systems as "Inspur/Inspur Power Systems" starting from 3Q 2018.