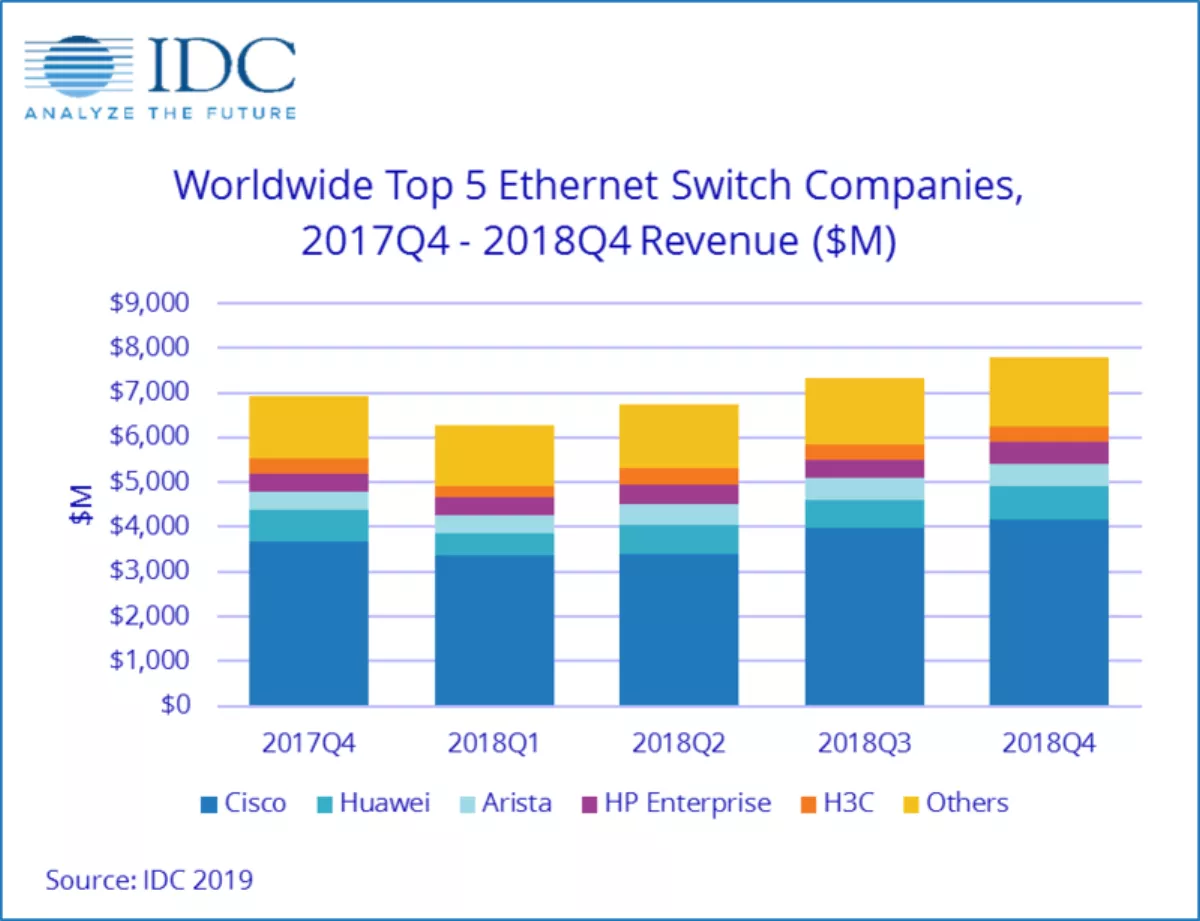

The worldwide Ethernet switch market (Layer 2/3) recorded USUS$7.8 billion in revenue in the fourth quarter of 2018 (4Q18), an increase of 12.7% year over year.

For the full year 2018, the market recorded US$28.1 billion in revenue for a year-over-year growth rate of 9.1%.

Meanwhile, the worldwide total enterprise and service provider router market recorded USUS$4.6 billion in revenue in 4Q18, increasing 15.6% on a year-over-year basis.

For the full year 2018, the router market finished at US$15.5 billion, an increase of 1.8% over 2017.

These results are according to the International Data Corporation (IDC) Worldwide Quarterly Ethernet Switch Tracker and Worldwide Quarterly Router Tracker.

The Asia/Pacific (excluding Japan) (APeJ) region increased 10.5% year over year in 4Q18 and grew 15.5% for the full year 2018.

"The Ethernet switching market saw solid growth around the world, driven by investments in both mature and emerging countries, indicating the strong demand for network infrastructure that powers enterprise Digital Transformation efforts," says IDC network infrastructure vice president Rohit Mehra.

"The market's strong fourth quarter helped push full year gains in Ethernet switching and sets the market up for continued strength in 2019, creating opportunities for vendors to capitalise on around the globe."

100Gb Ethernet switch revenue continues to grow rapidly as adoption by hyperscale cloud providers and large enterprises accelerates.

100GbE shipments reached more than 3.8 million ports and US$1.1 billion in revenue in 4Q18 and accounted for 13.6% of the full year's Ethernet switching revenue compared to 8.5% in 2017.

25Gb Ethernet switch products continue to see strong growth with port shipments rising 14.8% sequentially to 3.0 million and US$293.5 million in revenue in 4Q18.

The 10GbE market continues to see healthy growth but pricing pressure is holding back revenue increases.

10Gb port shipments in 4Q18 grew 14.6% year over year while revenues decreased 1.6% and made up 30.6% of all 2018 Ethernet switching revenues.

Meanwhile, 1Gb remains the primary connectivity technology for enterprise campus and branch deployments, driving 1Gb port shipments to 128.3 million in 4Q18, growing 12.7% year over year and making up 68.8% share of all ports shipped.

1GbE represented 41.8% of 2018 Ethernet switching revenues.

The worldwide enterprise and service provider router market grew 24.2% sequentially and 15.6% year over year in 4Q18 with the larger service provider segment rising 20.3% and the enterprise portion growing 2.2%.

For the full year, the combined market increased 1.8% with the service provider segment driving 2.0% growth and the enterprise segment growing 1.2%.

The combined enterprise and service provider router market saw growth around the world, with APeJ growing 22.4% year over year in 4Q18 and up 13.6% for the full year.

Cisco finished 4Q18 with a 13.2% year over year increase in Ethernet switching revenues and market share of 53.2%.

For the full year 2018, Cisco switching revenues rose 5.2% over 2017 while recording 52.8% market share (compared to 54.8% in 2017). In the hotly-contested 10GbE segment, Cisco remains the market leader, earning 48.5% of 10Gb revenues in 4Q18.

Cisco's combined service provider and enterprise router revenue increased 17.9% year over year in 4Q18, but was off 2.7% for the full year, giving the company 38.8% share in 2018.

Huawei's Ethernet switch revenue grew 6.0% year over year in 4Q18 for a market share of 9.7%. For the full year 2018, Huawei's Ethernet switch revenues grew 20.2%.

Huawei's enterprise and service provider router revenue increased 35.1% year over year in 4Q18 and rose 22.5% for the full year, giving the company 28.7% market share in 2018.

Arista Networks' Ethernet switching revenue rose 23.6% year over year and 28.5% in 2018. 100GbE revenues for Arista rose 6.6% sequentially in 4Q18 and were up 69.4% on the full year.

Arista's market share stood at 6.5% to end 2018, compared to 5.6% at the end of 2017.

Hewlett Packard Enterprise (HPE) revenues rose 20.2% year over year in 4Q18.

That led to a 16.5% year over year increase in 2018, putting the company's full year market share at 6.1% compared to 5.7% for 2017.

Juniper's Ethernet switch revenues declined 2.0% year over year in 4Q18 and were off 3.1% for the full year. Juniper's router revenues declined 12.7% year over year.

The company finished 2018 with 14.7% market share in the service provider routing market, down from 18.0% in 2017.